Sandals knowledge, sandals with community

Why the World in 2026 Puts Sustainability First: An Evidence-Based Analysis

Mar

Why the World in 2026 Puts Sustainability First: An Evidence-Based Analysis

Executive Summary

By 2026, multiple forces have converged to make sustainability a top priority worldwide.Rampant climate extremes record-breaking heat, floods, droughts and sea‑level rise have demonstrated the real-time impacts of global warming.Governments have responded with sweeping regulatory overhauls (from the EU’s Corporate Sustainability Reporting Directive to U.S. climate laws and China’s new ESG mandates) that are rapidly converting voluntary green pledges into legal requirements.Consumers especially younger generations are demanding green products, with surveys finding ~80–85% willing to pay a price premium for sustainable goods.Investors and capital markets are also shifting: global “sustainable” funds now command trillions in assets and green bond issuance hit record levels in 2024–25.In parallel, many corporations have set net-zero goals and begun restructuring supply chains (e.g. embracing circular economy practices and low-carbon technologies) in anticipation of these changes.

Simultaneously,resource constraints (water stress, mineral shortages) and new innovations (bio-materials, AI-driven efficiency) are reshaping costs and competitiveness.This report synthesizes evidence across climate science, policy, markets, and technology to explain why 2026 marks a turning point for sustainable business.Each section below highlights key statistics (from IPCC/WMO/UN and market reports) and includes practical implications for businesses.

Climate Impacts & Urgency (2018–2026)

Global warming has accelerated, with 2024 becoming the warmest year on record and each year from 2015–2024 ranking among the top ten hottest ever and carbon dioxide levels climbed to ~420 ppm in 2023 (151% of pre-industrial levels), driving extreme weather.Ocean heat content hit record highs in 2024, ice sheets are melting at unprecedented rates, and global sea level is rising faster (4.7 mm/year now vs. ~2.1 mm/year in the 1990s). These systemic changes have translated into devastating natural disasters. In 2024 alone, tropical cyclones, floods and droughts caused the highest number of climate-related displacements in 16 years Over 2002–2021, floods affected ~1.6 billion people ($832 billion in losses) and droughts impacted 1.4 billion ($170 billion).Notably,~50% of the world’s population now experiences severe water scarcity for at least part of each year, threatening agriculture and industry. In short, climate indicators are flashing red.

- Key Statistics: 2024 was the hottest year on record, with 10-year average temperatures at all-time highs. 2023 CO₂ = 420 ppm. Ocean and ice metrics at record extremes. Floods/droughts (2002–2022) affected >1.6 billion people. Half the global population faces water stress annually.

- Business Implications: 1.Climate risk management: Companies must integrate physical climate risks (floods, storms, heat) into their strategic planning and insurance models and 2.Supply chain resilience: Diversify and secure supply chains against weather shocks (e.g. alternative logistics, stockpiles) and 3.Product adaptation:Develop climate-resilient products and infrastructure (e.g. heat-tolerant agriculture, flood-proof facilities) to meet rising consumer and regulator expectations.

Policy & Regulatory Shifts (2020–2026)

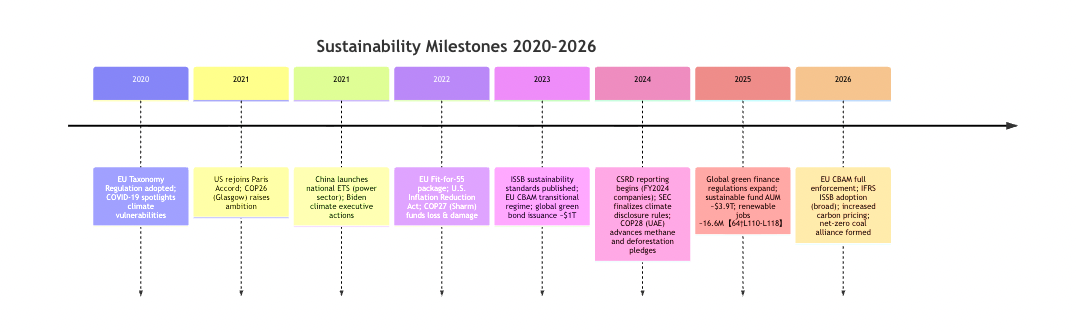

Since 2020, governments have dramatically tightened sustainability regulations worldwide.The EU leads with landmark laws: the Sustainable Finance Disclosure Regulation (SFDR), EU Taxonomy (defining “green” activities), and Corporate Sustainability Reporting Directive (CSRD), which requires around 50,000 companies to start ESG reporting for FY2024.From 2026 the EU’s Carbon Border Adjustment Mechanism (CBAM) will put a carbon price on imports.In the US, the 2022 Inflation Reduction Act directs ~$370 billion to clean energy and climate, while the SEC is finalizing mandatory climate disclosures.Meanwhile China launched its national carbon-trading system and moved ESG reporting from voluntary to mandatory (with new sustainability standards taking effect by 2025).

ASEAN economies are adopting green finance taxonomies and many countries are implementing Extended Producer Responsibility (EPR) for waste (e.g. plastics).Overall,carbon pricing coverage has surged: about 28% of global greenhouse gas emissions are now subject to a carbon price (from ~12% a decade ago).

| Region/Bloc | Key Regulatory Changes |

|---|---|

| European Union | CSRD (new ESG reporting, FY2024); EU Taxonomy (2020); SFDR fund disclosures; CBAM (full from 2026); Fit-for-55 climate package; stricter Packaging & Plastics EPR laws; expanded ETS coverage. |

| United States | Inflation Reduction Act (2022) funding renewables; SEC climate-disclosure rules (2024); executive climate orders; state carbon markets; possible Fed/Senate ESG guidance. |

| China | Carbon-neutrality pledge (2060) implemented via ETS (power sector launched 2021, expanding by 2025); mandatory ESG reporting standards (national guidelines for listed companies, 2025); Green Finance regulations. |

| Asia & Others | ASEAN Sustainable Finance Taxonomy (2022); Japan, Korea carbon pricing/ETS; Australia’s net-zero law; India’s clean energy targets; Global IFRS sustainability standards (ISSB) adoption planning. |

- Key Statistics: EU CSRD will affect ~50,000 companies from 2024.Carbon pricing now covers ~28% of global emissions. US climate investment (IRA) ~$370B; China’s ETS covers >3,000 companies by 2025.

- Business Implications: 1.Reporting compliance: Firms must upgrade data systems to meet new ESG disclosure requirements (CSRD, SEC/ISSB) or face penalties.2.Cost of carbon:Production inputs and supply chains will become more expensive as carbon taxes/ETS prices rise, incentivizing efficiency.3.Market access: Exporters into regulated markets (EU, UK) must demonstrate low-carbon products (CBAM) or face tariffs, driving investment into cleaner technologies.

Consumer Behavior & Market Trends

Consumer preferences have shifted markedly toward sustainability.Surveys reveal that ~85% of consumers feel the impacts of climate change in daily life and ~80–85% are willing to pay a premium for eco-friendly products.Remarkably,according to PwC, consumers would spend an average of9.7% moreon sustainably produced goods even amid inflation pressures.Younger generations lead this trend: a First Insight report found 62% of Gen Z shoppers prefer sustainable brands and 73% will pay morefor green products. A McKinsey survey on packaging reported 39% of respondents now rate environmental impact as “very important” nearly double the share in 2020. In practice, this means brands with clear sustainability credentials (organic/natural labels, carbon offsets, recycled materials) see rising market share.

- Key Statistics:85% of consumers globally cite direct effects of climate change; consumers will pay ~9.7% more on average for sustainable products. 62% of Gen Z prefer sustainable brands; 73% would pay a premium. In a global survey, 39% of people rank “environmental impact” as extremely/very important (2025) up from 20% (2020).

- Practical Implications:1.Product development:Companies should develop green product lines (e.g. sustainable packaging, eco-materials) to capture higher willingness-to-pay. 2.Marketing & branding:Authentic sustainability storytelling and certifications can build consumer trust and loyalty. 3.Customer engagement: Use digital platforms to highlight eco-efforts (carbon labels, recycling programs); engage younger consumers through social media and cause marketing.

Capital markets are also in the sustainability fast lane and Global issuance of green, social and sustainability bonds surpassed$1 trillionin 2024, with Bloomberg reporting ~$947 billion of green debt (bonds + loans) in 2025. Meanwhile,sustainable investment funds have exploded: assets under management in ESG‑branded funds rose from ~$1.4 trillion in 2018 to $3.6 trillion in 2024, and ~$3.9 trillion by mid-2025. Investor flows illustrate the trend: 2024 saw +$38 billion net inflow into sustainable funds, whereas 2025 saw a one-time dip (–$84 billion) – likely reflecting short-term market volatility.

Nonetheless,major asset managers and pension funds now routinely incorporate ESG factors; over 5,200 institutional investors (≈$140 trillion AUM) have signed the UN Principles for Responsible Investment. Notably, sustainable funds recently outperformed traditional funds, suggesting financial advantages to “doing well by doing good”. The green economy is also growing: low-carbon technologies and clean-energy companies are among the fastest-growing stock segments. For example, the “green economy” stock indexreached $7.9 trillion in market cap by Q1 2025 (8.6% of global equity) and has grown ~15% per year over the last decade – second only to tech.

| Instrument/Market | 2024 | 2025 | Source |

|---|---|---|---|

| Sustainable fund AUM | ~$3.6 trillion | ~$3.9 trillion | IFC-Amundi (2024); MS Research (mid-2025) |

| Net flows into sustainable funds | +$38 billion (net inflow) | –$84 billion (net outflow) | Morningstar/The Asset |

| Global green/SSS bond issuance | ~$1 trillion | ~$947 billion (bonds+loans) | IFC-Amundi; Bloomberg |

| Carbon pricing revenue | – | >$100 billion (2024) | World Bank (2024) |

- Key Statistics:Green bond/loan issuance hit ~$1 trillion in 2024. Sustainable fund assets ~3.6T in 2024, ~3.9T in 2025. Global carbon pricing now covers ~28% of emissions.

- Practical Implications:1.ESG reporting & disclosure: Enhanced transparency (e.g. TCFD/ISSB-aligned reports) is critical to attract capital and comply with emerging financial regulations. 2.Access to green finance: Companies should prepare to tap into cheaper green financing (green bonds, loans tied to ESG KPIs) and meet lender expectations on ESG performance. 3.Investor engagement: Expect greater scrutiny from shareholders and ratings agencies; proactive dialogue and verified sustainability claims can mitigate divestment and activism.

Corporate Adoption & Supply-Chain Shifts

Businesses are rapidly aligning with the green transition.A recent net-zero stocktake shows 63% of large global companies have set net-zero targets (mostly by 2050).So many more have interim goals (2030/2040 targets) and science-based commitments. Importantly, the shift requires rethinking supply chains: on average, a company’s Scope 3 emissions (from bought goods, logistics, etc.) are estimated to be 26× its direct operations emissions. Yet only ~15% of firms have concrete plans to address supply-chain emissions. Leading companies are moving to close this gap by working with suppliers on clean energy, using recycled inputs, and redesigning products for longevity and recyclability (circular economy). For example, automakers and electronics firms are investing in battery recycling programs, and apparel brands are implementing take-back and remanufacturing initiatives. Overall, aligning corporate strategy with a net-zero, circular model is becoming not just a moral choice but a business imperative.

- Key Statistics:63% of Forbes Global 2000 companies have net-zero carbon goals. Corporate supply-chain (Scope 3) emissions average 26× company direct emissions, yet only ~15% of companies set Scope 3 reduction targets.

- Practical Implications:1.Scope 3 integration: Measure and reduce upstream emissions by engaging major suppliers (energy use, materials, transport) – potentially through supplier scorecards and green procurement policies and 2.Circular strategies: Invest in product and packaging design for reuse/recycling (closing material loops) to meet new EPR/waste regulations and consumer demand and 3.Zero-carbon roadmaps: Establish clear plans (with interim milestones) toward net-zero targets, integrating low-carbon innovations (e.g. green hydrogen use, carbon capture) as needed.

Resource Constraints & Commodity Trends

The transition is set against tightening resource limits.Freshwater is under pressure: agriculture already accounts for ~70% of withdrawals, industry ~20%, and continued warming will intensify droughts and floods. Nearly half the global population endures water stress periodically, which can disrupt industries from manufacturing to energy and Critical minerals are another chokepoint: booming demand for lithium, cobalt, rare-earths (for EVs, batteries, electronics) risks supply bottlenecks.For example,Bloomberg projects rare-earth demand will outstrip new supply by 2030 (with China still dominating production).On the energy side, while fossil fuel demand remains high, investment flows increasingly favor renewables. (The COP28 agreement even set a target to triple renewable capacity by 2030.) Commodity price volatility (inflation, trade tensions) has made businesses more aware of resource risks.

- Key Statistics:~50% of people face water scarcity at least part of the year. Floods (2002–2022) caused ~$832 billion in losses. Rapid growth in EVs suggests battery minerals demand rising ~7%/yr (Bloomberg).

- Practical Implications:1.Efficiency & recycling:Implement aggressive water, energy and raw material efficiency measures and Reuse and recycle resources wherever possible (e.g. industrial water recycling, materials recovery) to hedge shortages and 2.Supply diversification: Source critical inputs from multiple suppliers and invest in recycling (e.g. recycled aluminum, circular plastics) to reduce reliance on geopolitically risky supplies and 3.Risk assessment: Factor resource risk into project economics (e.g. higher water costs, carbon taxes) and consider “waste = resource” strategies (e.g. waste heat recovery).

Technology & Innovation Enablers

Technological advances are unlocking new paths to sustainability and Materials innovation is accelerating: bio-based plastics (from plant oils, etc.) and advanced recyclables are reaching commercial scale.For instance, biobased polymers and recycled-content materials are growing in packaging and consumer goods and Energy technology is also transforming: solar and wind costs continue to fall, making renewables the cheapest new power in many regions.Grid-scale batteries, green hydrogen, and emerging storage are scaling up.

So digital technology plays a big role too.AI and data analytics now optimize energy use and logistics, and blockchain is used for supply-chain transparency (e.g. verifying carbon footprints).In finance, fintech and “AI for Earth” tools help investors analyze ESG risks and opportunities.As a result, the “green economy” is expanding rapidly: low-carbon companies now represent a growing share of market value.For example, global green stocks (renewables, EVs, batteries, etc.) were worth ~$7.9 trillion by Q1 2025 (8.6% of world equity market) and grew ~15%/yr on average and second only to tech stocks.

- Key Statistics:Sustainable packaging and eco-products saw ~28% cumulative growth over five years.The market cap of green-sector stocks reached $7.9 trillion (~15% CAGR). Renewable energy jobs topped 16.6 million in 2024.

- Practical Implications: 1.Adopt new materials Partner with suppliers of bio-based and recycled inputs (e.g. bioplastics, recycled steel) to differentiate products and 2.Digital adoption: Use AI and IoT for efficiency gains (smart manufacturing, predictive maintenance for energy reduction) and 3.Collaborate on innovation: Join consortia or public–private partnerships to scale emerging tech (e.g. carbon capture, renewable hydrogen) and stay ahead of regulation.

Economic Risks & Opportunities

Job creation is one big opportunity: green industries employ millions.In 2024, global renewable-energy jobs hit 16.6 million, with solar PV leading (7.3M jobs).China accounted for 7.3M of those jobs (44% of total), illustrating where new manufacturing is concentrated.Transition investments also spur local economies (e.g. clean energy factories, retrofitting projects).Financially, companies with strong ESG profiles have shown resilience: a Morgan Stanley report found sustainable funds outperforming peers in early 2025, and a CDP analysis showed ESG leaders had lower cost of capital.Conversely, “brown” sectors face writing downs (stranded coal or oil assets) and tightening investor scrutiny.Economists warn of transition risks: if action is too slow, climate damages could knock 4–5% off global GDP by 2100, whereas a smooth transition could add ~2% to GDP by 2030 via green growth.

- Key Statistics: Renewable energy workforce = 16.6 million (2024). Green sector market cap ~$7.9 trillion (2025). Studies estimate $7 trillion/year needed for global clean energy transition by 2030, presenting major investment opportunities.

- Practical Implications: 1.Skilling up: Invest in workforce training for green jobs (renewable installation, energy efficiency auditing, data analytics) to capitalize on new market opportunities and 2.Diversify business models: Explore services in sustainability (e.g. energy-as-a-service, sustainability consulting) to tap growth and 3.Anticipate disrund ption: Prepare for shifts (e.g. declining demand for petroleum-based products) by diversifying product lines and transitioning asset portfolios.

Action Checklist for Corporate Leaders

To translate these trends into business strategy, leaders should:

- Integrate Climate in Strategy:Embed climate risk assessments and sustainability metrics into core strategy and financial planning.

- Set Ambitious Targets:Adopt science-based emission/reduction targets (Scope 1, 2, and 3) and publicly commit to net-zero timelines.

- Enhance ESG Reporting:Build robust data systems to track and report ESG performance (aligned with CSRD/SEC/ISSB) and verify claims with third-party audits.

- Optimize Operations:Cut energy and resource use (e.g. by improving process efficiency, switching to renewables, water recycling) to reduce costs and emissions.

- Rethink Supply Chains:Map Scope 3 hotspots, engage suppliers on low-carbon solutions, and diversify sources to manage resource risks (e.g. alternative materials).

- Adopt Circular Practices:Design products for durability and recyclability, implement reuse or take-back programs, and reduce waste in production.

- Invest in Innovation:Allocate R&D to green technologies (clean energy, sustainable materials, carbon capture) and pilot emerging solutions.

- Seek Sustainable Finance:Explore green loans and bonds, and meet lender/investor ESG criteria to lower financing costs.

- Engage Stakeholders:Communicate sustainability efforts transparently to investors, customers, and regulators; involve employees in green initiatives to build culture.

- Monitor & Adapt:Stay abreast of policy changes (e.g. new regulations or incentives) and update strategies accordingly.

In 2026, sustainability is no longer optional it’s a core driver of competitiveness and long-term success.

Sources:Authoritative data and reports from WMO, UNESCO, IPCC, EU Commission, World Bank, Morgan Stanley, IRENA, and major market research (PwC, McKinsey, etc.) are cited above to support all statements and statistics.

ทำไมโลกในปี 2026 จึงให้ความสำคัญกับ “ความยั่งยืน (Sustainability)” มากขึ้น

วิเคราะห์จากข้อมูลจริงของเศรษฐกิจโลก ธุรกิจ และพฤติกรรมผู้บริโภค

ในช่วงไม่กี่ปีที่ผ่านมา คำว่า Sustainability หรือ ความยั่งยืน ไม่ได้เป็นเพียงเทรนด์ด้านสิ่งแวดล้อมอีกต่อไป แต่กำลังกลายเป็น “โครงสร้างหลักของเศรษฐกิจโลก” ที่กำหนดทิศทางธุรกิจ การลงทุน และพฤติกรรมผู้บริโภคอย่างชัดเจน โดยเฉพาะในปี 2026 ที่หลายองค์กรทั่วโลกเริ่มมองว่า Sustainability ไม่ใช่ทางเลือก แต่คือ “เงื่อนไขของการอยู่รอด” ในระยะยาว

การเปลี่ยนแปลงนี้ไม่ได้เกิดขึ้นเพราะกระแสสังคมเพียงอย่างเดียว แต่เป็นผลจากการบรรจบกันของหลายปัจจัย ทั้งวิกฤตสภาพภูมิอากาศ กฎหมายใหม่ด้าน ESG การเปลี่ยนแปลงของตลาดทุน และความคาดหวังของผู้บริโภครุ่นใหม่ ซึ่งกำลังสร้างระบบเศรษฐกิจรูปแบบใหม่ที่เรียกว่า Sustainable Economy

บทความนี้จะอธิบายให้เห็นอย่างชัดเจนว่า เหตุใดโลกในปี 2026 จึงให้ความสำคัญกับความยั่งยืนมากกว่าที่เคย และสิ่งนี้หมายความว่าอะไรสำหรับธุรกิจ รวมถึงอุตสาหกรรมแฟชั่นและรองเท้าอย่าง Sandals World

โลกกำลังเผชิญผลกระทบ Climate Change แบบ “เรียลไทม์”

หนึ่งในเหตุผลสำคัญที่สุดที่ทำให้ Sustainability กลายเป็นวาระหลักของโลก คือหลักฐานทางวิทยาศาสตร์ที่ชัดเจนขึ้นทุกปี

ข้อมูลจากองค์กรด้านภูมิอากาศระดับโลกพบว่า

-

ปี 2024 เป็นปีที่ร้อนที่สุดเท่าที่เคยบันทึกมา

-

ระดับก๊าซ CO₂ ในชั้นบรรยากาศสูงถึงประมาณ 420 ppm ซึ่งมากกว่าก่อนยุคอุตสาหกรรมกว่า 150%

-

ระดับน้ำทะเลเพิ่มขึ้นเร็วกว่าในทศวรรษ 1990 มากกว่าสองเท่า

-

เกือบครึ่งหนึ่งของประชากรโลกเผชิญภาวะขาดแคลนน้ำในบางช่วงของปี

ผลกระทบเหล่านี้ไม่ได้อยู่ไกลตัวอีกต่อไป แต่เริ่มกระทบห่วงโซ่อุปทาน การเกษตร การผลิต และต้นทุนธุรกิจโดยตรง น้ำท่วม ภัยแล้ง และคลื่นความร้อนทำให้บริษัททั่วโลกต้องเริ่มประเมิน “Climate Risk” เป็นส่วนหนึ่งของกลยุทธ์องค์กร

นั่นหมายความว่า Sustainability ไม่ใช่เรื่องภาพลักษณ์ แต่เป็นเรื่อง การบริหารความเสี่ยงทางธุรกิจ

กฎหมาย ESG และ Sustainability กำลังเปลี่ยนจาก “สมัครใจ” เป็น “ข้อบังคับ”

ตั้งแต่ปี 2020 เป็นต้นมา โลกได้เห็นการเปลี่ยนแปลงด้านกฎระเบียบครั้งใหญ่ที่สุดเกี่ยวกับความยั่งยืน

สหภาพยุโรปออกกฎหมายสำคัญ เช่น

-

Corporate Sustainability Reporting Directive (CSRD)

-

EU Taxonomy

-

Carbon Border Adjustment Mechanism (CBAM) ที่เริ่มใช้เต็มรูปแบบในปี 2026

กฎหมายเหล่านี้บังคับให้บริษัทหลายหมื่นแห่งต้องรายงานข้อมูล ESG อย่างโปร่งใส และสินค้าที่ปล่อยคาร์บอนสูงอาจถูกเก็บภาษีเพิ่มเมื่อเข้าสู่ตลาดยุโรป

ในขณะเดียวกัน สหรัฐอเมริกา จีน และประเทศในเอเชียก็เริ่มใช้มาตรฐานรายงานด้านความยั่งยืนเช่นกัน ส่งผลให้ Sustainability กลายเป็น “มาตรฐานการค้าโลกใหม่”

สำหรับธุรกิจแฟชั่นและรองเท้า สิ่งนี้หมายความว่า

วัสดุ กระบวนการผลิต และซัพพลายเชน จะถูกตรวจสอบมากขึ้นกว่าที่เคย

ผู้บริโภคยุคใหม่เลือกแบรนด์ที่มีความยั่งยืน

การเปลี่ยนแปลงไม่ได้เกิดจากภาครัฐเท่านั้น แต่เกิดจากผู้บริโภคเอง

ผลสำรวจระดับโลกพบว่า

-

ประมาณ 85% ของผู้บริโภครู้สึกถึงผลกระทบของ Climate Change ในชีวิตจริง

-

ผู้บริโภคยอมจ่ายเพิ่มเฉลี่ยเกือบ 10% สำหรับสินค้าที่ผลิตอย่างยั่งยืน

-

62% ของ Gen Z เลือกซื้อจากแบรนด์ที่มี Sustainability ชัดเจน

นี่คือจุดเปลี่ยนสำคัญ เพราะ “คุณค่าของสินค้า” ไม่ได้วัดแค่ดีไซน์หรือราคาอีกต่อไป แต่รวมถึงผลกระทบต่อโลก

แบรนด์ที่สามารถเล่าเรื่องการผลิตอย่างรับผิดชอบ เช่น การใช้วัสดุ Bio-based หรือการผลิตแบบ Handmade ที่ลดการผลิตเกินความจำเป็น จึงเริ่มได้รับความสนใจมากขึ้น

เงินลงทุนทั่วโลกกำลังไหลเข้าสู่ Sustainable Business

อีกแรงผลักดันสำคัญคือภาคการเงิน

ตลาดพันธบัตรสีเขียว (Green Bond) มีมูลค่าเกิน 1 ล้านล้านดอลลาร์ต่อปี ขณะที่กองทุน ESG มีสินทรัพย์รวมเกือบ 4 ล้านล้านดอลลาร์ภายในปี 2025

นักลงทุนเริ่มมองว่า บริษัทที่มี ESG ดีมีความเสี่ยงต่ำกว่าในระยะยาว เพราะสามารถรับมือกฎระเบียบและความเปลี่ยนแปลงของตลาดได้ดีกว่า

ผลลัพธ์คือ ธุรกิจที่ไม่ปรับตัวด้าน Sustainability อาจเข้าถึงเงินทุนได้ยากขึ้นในอนาคต

บริษัททั่วโลกกำลังเปลี่ยน Supply Chain สู่ Net Zero

ปัจจุบันกว่า 60% ของบริษัทขนาดใหญ่ทั่วโลกประกาศเป้าหมาย Net Zero แล้ว

สิ่งที่หลายองค์กรค้นพบคือ การปล่อยคาร์บอนส่วนใหญ่ไม่ได้มาจากโรงงานของตัวเอง แต่เกิดจากซัพพลายเชน หรือที่เรียกว่า Scope 3 Emissions ซึ่งอาจสูงกว่าการดำเนินงานภายในถึง 26 เท่า

จึงเกิดการเปลี่ยนแปลงสำคัญ เช่น

-

ใช้วัสดุรีไซเคิล

-

ลดการผลิตเกิน

-

ออกแบบสินค้าให้ใช้งานได้นานขึ้น

-

ส่งเสริม Circular Economy

แนวคิดนี้สอดคล้องกับแบรนด์รองเท้าในเครือ Sandals World ที่เน้นงานแฮนด์เมดและการผลิตอย่างมีความรับผิดชอบ ซึ่งช่วยลดการผลิตแบบ Mass Waste ได้โดยธรรมชาติ

ทรัพยากรโลกกำลังตึงตัว ทำให้ Sustainability กลายเป็นเรื่องเศรษฐกิจ

ความยั่งยืนไม่ได้เกิดจากอุดมการณ์เพียงอย่างเดียว แต่เกิดจากข้อจำกัดของทรัพยากร

ปัจจุบัน

-

ภาคเกษตรใช้น้ำประมาณ 70% ของโลก

-

ความต้องการแร่สำหรับแบตเตอรี่และพลังงานสะอาดเพิ่มขึ้นอย่างรวดเร็ว

-

ราคาพลังงานและวัตถุดิบผันผวนสูง

ธุรกิจจึงเริ่มตระหนักว่า “ประสิทธิภาพทรัพยากร” คือความได้เปรียบทางการแข่งขัน

การใช้วัสดุชีวภาพ เช่น BIO EVA หรือวัสดุจากพืช จึงไม่ใช่แค่รักษ์โลก แต่ช่วยลดความเสี่ยงต้นทุนในอนาคต

เทคโนโลยีใหม่กำลังเร่งโลกเข้าสู่ Sustainable Economy

นวัตกรรมด้านวัสดุและพลังงานทำให้ Sustainability กลายเป็นสิ่งที่ทำได้จริง

ตัวอย่างเช่น

-

วัสดุ Bio-based และรีไซเคิลเชิงอุตสาหกรรม

-

พลังงานหมุนเวียนที่มีต้นทุนต่ำลง

-

AI ที่ช่วยลดพลังงานในการผลิต

-

Blockchain สำหรับตรวจสอบซัพพลายเชน

เศรษฐกิจสีเขียวมีมูลค่าตลาดเกือบ 8 ล้านล้านดอลลาร์ และเติบโตเฉลี่ยประมาณ 15% ต่อปี ซึ่งใกล้เคียงอุตสาหกรรมเทคโนโลยี

ความยั่งยืนคือโอกาสทางเศรษฐกิจ ไม่ใช่ต้นทุน

หลายคนยังมองว่า Sustainability คือค่าใช้จ่าย แต่ข้อมูลกลับชี้ตรงกันข้าม

อุตสาหกรรมพลังงานหมุนเวียนสร้างงานกว่า 16 ล้านตำแหน่งทั่วโลก และธุรกิจที่มี ESG แข็งแรงมักมีต้นทุนเงินทุนต่ำกว่า

นักเศรษฐศาสตร์ประเมินว่า หากโลกเปลี่ยนผ่านสู่เศรษฐกิจสีเขียวได้สำเร็จ อาจช่วยเพิ่ม GDP โลกได้ในระยะยาว

ดังนั้น Sustainability จึงกลายเป็นทั้ง “กลยุทธ์ลดความเสี่ยง” และ “เครื่องยนต์การเติบโตใหม่”

ปี 2026 คือจุดเปลี่ยนของโลกธุรกิจ

เหตุผลที่โลกในปี 2026 ให้ความสำคัญกับ Sustainability มากขึ้น ไม่ได้เกิดจากกระแสเพียงชั่วคราว แต่เกิดจากการรวมตัวของ 5 แรงขับหลัก ได้แก่

-

วิกฤต Climate Change ที่เห็นผลจริง

-

กฎหมาย ESG ที่เข้มงวดขึ้นทั่วโลก

-

ผู้บริโภคเลือกแบรนด์ที่รับผิดชอบต่อโลก

-

เงินลงทุนไหลเข้าสู่ธุรกิจยั่งยืน

-

เทคโนโลยีใหม่ทำให้การเปลี่ยนผ่านเกิดขึ้นได้จริง

สำหรับอุตสาหกรรมรองเท้าและแฟชั่น รวมถึงเครือพันธมิตร Sandals World การพัฒนาไปสู่ Sustainable Design, Responsible Materials และ Ethical Craftsmanship ไม่ใช่เพียงการสร้างภาพลักษณ์ แต่คือการวางรากฐานธุรกิจในเศรษฐกิจยุคใหม่

เพราะในโลกปี 2026 ความยั่งยืนไม่ได้เป็นทางเลือกอีกต่อไป แต่คือมาตรฐานใหม่ของความสำเร็จทางธุรกิจ

#Sandalsworld #รองเท้าartandcraft #รองเท้าแตะสานแฮนด์เมด #artandcraftsandals #artistichandmadesandals #handmade #artandcraft #sandals #รองเท้าแฮนด์เมด #รองเท้าแตะใส่แล้วไม่ลื่น #รองเท้ายางพารา #ใส่ไปไหนก็ได้

บทความโดย

Art and craft sandals by Sandalsworld thailand.

ABOUT THE CONTENT CREATOR

BUNTHARIK INSIRI

(Content Writer)

The Largest HubArtistic Handmade Sandals

BY

SANDALS WORLD THAILAND

of Artistic Handmade Sandals in Thailand.